Hillbreak is delighted to confirm that Sophie Carruth, formerly European Head of Sustainability at LaSalle, has joined its team to concentrate on the delivery of ESG training and education services to its clients globally.

Her arrival follows the recent appointments of veteran ESG data standards and reporting specialist, Matthew Tippett, and former Magic Circle lawyer, Jessica Moore as governance and regulatory specialist.

Carruth was responsible for driving ESG into the heart of LaSalle’s real estate investment activities in Europe. She developed and oversaw the delivery of LaSalle’s European Sustainability Strategy, focusing on the four pillars of climate change, responsible consumption, rewilding and social value. She was responsible for driving the creation of LaSalle’s first Net Zero Carbon Pathway, which embeds the management of ESG at each stage of the asset lifecycle.

Carruth was the longest-serving member of LaSalle’s Global Sustainability Committee and led the delivery of ESG education across the business, which included a collaboration with Hillbreak to provide ESG Training to its European leadership team in 2020.

Until leaving LaSalle, Carruth was a board director at the Better Buildings Partnership and chaired its ESG Training Steering Group, which oversaw the appointment and supervision of Hillbreak to deliver the ground-breaking BBP ESG Training for Real Estate Professionals. She was also a Steering group member for the IPF research project: ESG Benchmarking in Real Estate, and was a Member of INREV Sustainability Committee from 2014–2016. She continues as a Member of the Women in Sustainability Network.

Carruth comes from an asset management background at LaSalle and is a Member of the Royal Institution of Chartered Surveyors. She completed her Masters in Real Estate Management at London South Bank University and before that gained a BA (Hons) in French and Italian at Bristol University.

With demand for Hillbreak’s industry-leading ESG training and education growing in all of the major global markets, Carruth will focus exclusively on developing and delivering learning support to clients that are seeking to enhance both the knowledge and the practical skills needed to address investment and corporate imperatives in this rapidly developing area. She will play an instrumental role in further developing and delivering the hugely successful BBP ESG Training course, as well as bespoke learning programmes for individual client organisations.

Commenting on her arrival, Jon Lovell, Co-Founding Director of Hillbreak, said:

“We’re delighted to welcome Sophie to Hillbreak. She’s so well regarded amongst her peers for the impact she’s had over many years in the real estate industry and I know our clients will benefit greatly from her deep and extensive experience. She’s a natural leader and teacher; her instinct for mentoring others on their own ESG journeys is something that’s really stood out to me over the years that we’ve known each other. She’s a perfect fit for our expanding training business.”

Miles Keeping, also Co-Founding Director, added:

“As we head into 2022 – another pivotal year for our own business and the industry more widely – there’s no-one we’d rather be working with to further our ESG training and education services. We know from the feedback we’ve already had from clients with whom Sophie will be working that she’ll be an absolute hit with them and we feel really privileged to be working with her.”

Carruth said:

“I’m excited to join the Hillbreak team to deliver much needed ESG training to the real estate sector. There is a huge need to upskill property professionals so it’s great to be part of the solution and help as many people as possible from all aspects of the industry to integrate a better understanding of sustainability into their working practices.”

https://www.hillbreak.com/wp-content/uploads/2022/01/sophie-bw.png15861052Timia Berthoméhttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngTimia Berthomé2022-01-10 08:14:042022-05-05 22:48:45Sophie Carruth joins Hillbreak from LaSalle

Hillbreak has strengthened its team with the appointment of veteran ESG data standards and reporting specialist, Matthew Tippett, and former Magic Circle lawyer, Jessica Moore.

Tippett joins forces with the firm having spent twenty years at Upstream and JLL, where he latterly became National Director responsible for sustainability performance measurement, data management, benchmarking, quality assurance, corporate disclosure & reporting and net zero transition pathways.

During his career to date, he has been instrumental in defining several real estate industry standards for measurement and reporting of non-financial data, including the GRI Construction and Real Estate Sector Supplement, the EPRA Best Practice Recommendations for Sustainability Reporting (sBPR) and the Global Real Estate Sustainability Benchmark (GRESB) assessment.

Moore spent seven years as a lawyer, mostly at Magic Circle firm Freshfields. She specialised in financial crime such as fraud, money laundering, corruption and regulatory disputes, advising governments, financial institutions and corporates, in the UK and abroad. She has since complemented her legal background with several years of applied conservation work at the Royal Botanic Gardens at Kew, including developing in-depth knowledge of the complexities of carbon offsetting and nature-based solutions.

The arrival of Tippett and Moore adds further gravitas to Hillbreak’s role as a critical friend and training partner on ESG matters to many of the world’s preeminent asset managers and investors.

Tippett is expected to play a pivotal role in guiding clients as they plan and execute their transparency obligations, including navigating the complex landscape of reporting standards and the plethora of related ESG data management solutions.

Moore is advising global asset managers and premium listed entities on a range of strategic matters, whilst also supporting investors’ stewardship and engagement activities with third party asset managers.

Commenting on their appointments, Jon Lovell, Hillbreak co-founder, said:

“Miles and I are so pleased to welcome Matthew and Jess to the Hillbreak family. Matthew is someone we’ve known and admired for nearly two decades; clients and peers alike have the utmost respect for his integrity and the outstanding contribution he’s made to the advancement of ESG within the real estate industry. Jess brings exceptional rigour and thoughtfulness on matters of corporate governance, particularly in the context of the rapidly evolving global landscape of financial regulation affecting both public and private markets.”

Miles Keeping added:

“We’re delighted by the reaction we’ve already had from clients to the arrival of Matthew and Jess. Their immediately positive feedback has validated our view that they bring best-in-class capabilities to the firm which further enhances our distinctive offering as a completely independent, strategic advisor to the senior leadership teams of acclaimed clients.”

Tippett, who started working with Hillbreak this week, said:

“Joining Hillbreak is brilliant on many fronts: for me — I’m going to learn so much from the diverse and deep expertise of the team. For the team and its clients — I am extremely excited and enthused to contribute and combine my measurement and reporting knowledge with all of Hillbreak’s leading capabilities so as to help organisations accelerate their journeys to deeper and truer sustainability.”

Moore, a recent joiner, commented:

“I am hugely privileged to join the exceptional Hillbreak team at this critical and dynamic moment for ESG and climate finance. It’s exciting to be working with colleagues of such standout quality and depth of expertise. And I feel completely uplifted to be in harness alongside ambitious clients whose leadership is driving globally-significant change and shifting the entire market baseline in the process.”

https://www.hillbreak.com/wp-content/uploads/2020/02/hillbreak-leadership-role.jpg7231200Craig Clarkhttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngCraig Clark2021-09-15 18:02:082021-09-16 12:19:51Hillbreak Appoints Tippett & Moore

Revolutions are born of systemic crises. Amongst systemic crises, planetary breakdown is the ultimate. In response, ESG is seeking to remake the world anew. Mark Carney has called for a revolution in economic theory to respond to the market failure of climate change. The Financial Stability Board is the revolutionary council: the founding charter, the Recommendations of its Taskforce for Climate-related Financial Disclosures (‘TCFD’).

Revolutions are disruptive, but not invariably destructive: many effect positive change. But overturning the ancien régime is only the beginning. Most revolutions fight a civil war over the meaning of the movement.

The product of multiple disparate insurgencies, ESG emerged as a many splintered thing. There has been no agreement on the language of “sustainable”, “green”, or “responsible” investment. The time from Year Zero to Net Zero is foreshortened: phenomena modelled for the end of the century are being observed today. Consequently, the new movement has to establish governance without a full sheaf of foundational documents in place.

The greatest risk to the movement’s credibility is the struggle for transparency. ESG is confronting the vulnerability to fraud that it shares with any area where large sums of money flow into a less than entirely clear pool. Improved data and greater scrutiny are having an impact: earlier this year the Global Sustainable Investment Alliance chronicled a drop of $2trn in European AUM from 2018-2020, due to “significant changes in the way sustainable investment is defined” in that part of the world.

But ESG is a global revolution and, in the absence of a universal language, investors have struggled to pin down the terminology. In 2020, Common Wealth found that of 33 funds marketed as climate-themed, 12 held oil and gas producers. Last month, InfluenceMap reported that of 130 “climate” funds, a majority were not Paris-aligned, with many holding fossil fuel assets. The report flagged a widespread “lack of consistency and clarity” around ESG labelling, making it hard to determine “what these funds’ descriptors mean in practice”.

Won’t get fooled again

A new constitution may anchor accountable government. TCFD both stands alone and underpins many authorities’ frameworks. Regulators in the UK, Hong Kong, Singapore and China are in various stages of aligning TCFD disclosures into reporting cycles. The EU is warier and has developed a more independent framework. Its technical armoury, whilst very much still in beta, is nonetheless more sophisticated than anyone else’s. Unlike the principles-based TCFD, the EU’s characteristic micro-managing adds value in this case by confronting head-on ESG’s critical definitional issues. Its signature Taxonomy issues technical criteria for assessing whether business activities can be considered “sustainable”. Controversy around the appropriateness and efficacy of those criteria has delayed its implementation, and will continue after the additional measures are published.

Another brick in the wall fell into place this year: EU regulated firms, and those marketing in the EU, are now caught by the Sustainable Finance Disclosure Regulation (‘SFDR’), which focusses specifically on requiring firms to substantiate their claims. Both the SFDR and the TCFD codify credibility, requiring companies to weave sustainability into the fabric of their investment and strategic decisions, risk assessments and incentive plans. Being able to demonstrate such structuralised sincerity is likely to be a core element of any defence for a company facing greenwashing prosecutions.

The US is late to a war fought largely on European turf and is unusually underequipped. It has not yet revised its patchy and outdated Names Rule and is still drafting its climate disclosure requirements. These new regulations aim at consistency and comparability for investors; they may include scenario planning (echoing the TCFD), but full Scope 3 emissions disclosures are meeting resistance.

This summer, though, the US made an explosive entrance. Its Securities and Exchange Commission (‘SEC’) joined Germany’s BaFin in investigating allegations that Deutsche Bank’s DWS Group overstated the ESG credentials of its products. As a foreign operative, DWS presents an opportunity for the SEC to show some muscle without taking a swipe at US businesses – which will nonetheless heed the warning. Co-ordinating with BaFin will allow the SEC to learn from Europe’s more established thinking on ESG matters. The SEC may also draw on the EU’s greater statutory toolkit, while its own is undeveloped. The US’s financial dominance means its role will be decisive through sheer numbers: if this early skirmish with DWS helps it crystallise its strategy, it could be a critical moment.

America famously holds certain truths to be self-evident. The SEC has understood that specific regulation is not essential for combatting greenwashing. Good old-fashioned truthfulness remains a powerful principle, as manifested variously worldwide. This will be critical for the DWS prosecution, as the allegations against it relate to the period before the SFDR came into force. The key charge against DWS is that it claimed more than half its assets were invested using ESG criteria, when it is alleged that in practice portfolio managers had no obligation to act upon ESG data. In July the UK’s Financial Conduct Authority had made the point explicitly, setting out those existing transparency obligations which are breached by greenwashing. The letter noted that formal fund documents “often contain claims that do not bear scrutiny”; it reminded asset managers to “describe their investment strategies clearly” and ensure that “any assertions made about their goals are reasonable and substantiated”. The guidance is expected to be formalised in legislation.

The universality of the honesty principle allows a breadth of greenwashing action beyond specialised financial regulators. It was the Netherlands’ Advertising Code Committee which ruled last month that Shell’s ‘Drive carbon neutral’ campaign was misleading. Even in Australia’s regulatory desert, the judicial system tests companies’ integrity: its Federal Court will weigh the assertion of Santos Ltd that natural gas provides “clean energy”. Interestingly, it will also consider the credibility of a “net zero” pathway which leans heavily on distinctly inchoate carbon capture and storage technology: the oil and gas sector will be watching.

ESG’s associated guardians are similarly under pressure to make their language meaningful. The Financial Reporting Council, stung by criticism of its rigour, revised its Stewardship Code this month, ejecting Schroders, Morgan Stanley IM and Rothschild Wealth Management in the process. The International Financial Reporting Standards foundation is accelerating its ESG reporting recommendations, hopefully in time for COP26. The ratings agency MSCI was criticised for giving Boohoo a high ESG rating despite its labour conditions scandal; complaints about low ratings from companies such as ExxonMobil may be less justified. Many sustainable ETFs track MSCI ESG indices (including DWS’s rebranded ETF) but MSCI defends its ESG ratings as opinions, as distinct from credit ratings. Since those credit ratings escaped regulation after the financial crash, their ESG counterparts seem unlikely to draw fire any time soon. The quality of carbon offsetting is also a live issue, with doubts in particular over the additionality of certain certified projects. Offsetting continues to evolve, helped by a widespread commitment to transparency across the industry.

The revolution rolls out across the wider economy. The EU Taxonomy applies also to non-financial companies. UK premium listed companies must report in line with the recommendations of the TCFD. This particularly is a powerful development: the globalised nature of many London-listed businesses means that regional climate regulations are beginning to be internationalised. The transparency obligations increasingly being placed on public companies are believed to be a significant factor in various recent take-private manoeuvres.

There remain battles to be fought. The TCFD’s 2020 Status Report noted that pure metrics are insufficiently accompanied by context around their significance. At the same time, users of TCFD disclosures identify exactly that material as the most useful, as it reveals a company’s resilience to climate-related changes. As an example, various regimes require companies to disclose their emissions, but the TCFD expects those data to be used intelligently in scenario planning. For instance, how might a large emissions footprint harm the company’s financial situation as the price of carbon (which hit a record €61 at the end of August) continues to increase?

Children of the revolution

ESG is not the anti-capitalist creed that some allege: its champions are titans of industry and finance such as Bill Gates, Larry Fink and Hiro Mizuno. That is not to say there will be no purges; heads rolled at ExxonMobil earlier this year due to the Board’s refusal to recognise that the times they are a-changing. But ESG’s constructive dialogue with the existing regime suggests a peaceful transition ultimately.

Hillbreak is confident that ESG will find the ‘stable’ in ‘sustainable’. ESG is not the real wild child that, say, crypto is. “Green finance” is essentially just “finance”: the fundamentals of integrity are no different. Regulation forms the bones of the body politic, but governance must flesh it out. Irrespective of whether COP26 delivers any international standardisation, the direction of travel is clear. The mere allegation of greenwashing caused DWS’s share price to fall over 13%. Reputational impact occurs quicker, and often lasts longer, than formal proceedings.

The new philosophy is only strengthened with testing. Where clients have concerns about how to engage with it, Hillbreak stands ready as a critical friend, but time is running out for companies wanting to be on the right side of history. Vive la révolution!

https://www.hillbreak.com/wp-content/uploads/2021/09/highway-2025863_640.jpg426640Jessica Moorehttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngJessica Moore2021-09-07 17:57:232023-02-27 20:21:27Talkin’ ’bout a revolution: greenwash in the firing line

The Better Buildings Partnership (BBP) is today launching a major real estate industry training course focused on integrating Environmental, Social & Governance (ESG) into the property investment management process. The launch of the much-anticipated course comes just months after Sarah Ratcliffe, CEO at BBP, declared a sustainability skills emergency within the sector and encouraged the use of appropriate leadership and infrastructure to bridge the knowledge gap.

The training course has been envisioned by BBP members and will be developed and delivered by Hillbreak, a market leading ESG training and advisory firm.

The ground-breaking new course has been developed especially for real estate professionals working for fund management and investment advisory institutions, Real Estate Investment Trusts and private property companies. The programme will bring together participants from varied roles, such as fund, asset and development management, deal teams, investor relations and product development, thereby maximising the level of insight that can be gained from interacting with peers working across the spectrum of the property lifecycle.

The course comes at a very significant time for the real estate sector with the climate crisis and ESG now firmly established as priorities for investors, owners, occupiers and other stakeholders. Participants will benefit from having a better command of how to respond to the ESG risks and opportunities that will increasingly impact upon their decision-making, and have a better understanding of the principles, disciplines and tools required to develop strategies and solutions for their portfolios and assets.

The training involves two half-days of interactive teaching supported by preparatory and post-course learning delivered via a dedicated online platform. Learning materials and formats will include classroom-style learning, interview-based video and podcast content, together with written resources and case studies. There will be bespoke materials specific to role types, ensuring maximum relevance to the individual and their organisations.

The first training course will take place in June and class sizes are limited to optimise peer-to-peer learning through real-world insights.

To find out more about the course, and to register for places, please visit the Hillbreak website here.

Louise Ellison, Chair of the BBP and Group Head of Sustainability at Hammerson said:

“Access to targeted, practical ESG training that focuses on equipping people with expertise they can deploy directly within their roles is essential for our sector to move forward quickly on climate change. This programme provides an excellent response so I am really delighted to have been part of its development and to see it launched.”

Sophie Carruth, Head of Sustainability at LaSalle Investment Management said:

“A key tool in the delivery of Net Zero Carbon is the upskilling of the people in each sector so I am excited to see the launch of this ESG training which we designed specifically for property professionals. I believe it will be hugely impactful and will drive progress across our sector”

Miles Keeping, co-Founder of Hillbreak and Chair of the Green Property Alliance said:

“It’s very exciting to be able to bring this much needed training initiative to the market. Hillbreak was formed to help meet the significant need for ESG training and we’re delighted to have the opportunity to partner with the BBP on this ground-breaking programme.”

Notes to Editors

About BBP

The Better Buildings Partnership (BBP) is a not-for-profit collaboration of the UK’s leading property owners who are working together to improve the sustainability of the UK’s existing commercial buildings. The organisation’s aim is to deliver market transformation through sustainability leadership and knowledge sharing across the UK property industry. The BBP currently has 40 members who represent in excess of £250bn Assets Under Management (AUM). More information about the BBP can be found here: www.betterbuildingspartnership.co.uk

About Hillbreak

Hillbreak delivers impactful training and advisory services for organisations seeking purpose and competitive advantage in a rapidly changing world. Its mission is to expedite the transition to a sustainable policy, business and investment environment by bringing intelligence, challenge and inspiration to its clients and stakeholders. Please see www.hillbreak.com for further information about Hillbreak.

For press enquiries please contact Sophia Tysoe, Stakeholder Engagement and Communications Executive, Better Buildings Partnership. s.tysoe@betterbuildingspartnership.co.uk

https://www.hillbreak.com/wp-content/uploads/2021/02/paris-1309397_640.jpg426640Timia Berthoméhttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngTimia Berthomé2021-02-25 05:00:122021-02-23 17:40:06Better Buildings Partnership launches groundbreaking ESG Training Course for Real Estate Professionals

Regulators and investors alike are increasingly signing up to the theory that for investments to be considered well managed, they must manage all the relevant risks, including environmental and social factors. For this to be done, these risks must be both well-articulated (and thanks to the likes of TCFD, the EU, the UN and the GIIN this is increasingly so) and well-priced.

This means that it is inevitable that measurement of the sustainability and impact of investments will apply to all, and not just those emerging products which were once considered niche.

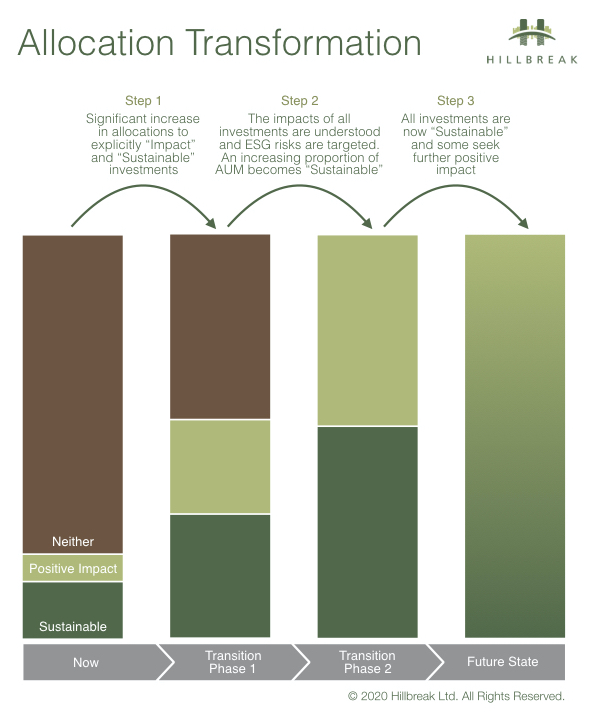

Thanks to the emerging regulation and market consensus around the definitions, investors can now begin to look again at their portfolios and determine which of their investments are:

Good enough – genuinely sustainable, meaning doing no harm and adequately addressing specific environmental and social risks;

Improving – having a measurable, positive impact in terms of reducing, managing or mitigating environmental and social risk. Note that these two categories are not mutually exclusive; or

Not good enough / unknown – either having a negative impact, or unable to articulate and measure their impact and therefore not able to adequately manage or mitigate environmental and social risks.

The journey all responsible investors must go on should involve a transformation of their allocations using these lenses, as shown below.

Governance and oversight

The evolution of the governance and oversight of investments is already underway. Regulators have been highlighting the extent to which banks and insurers are exposed to environmental risk[1], and have begun stress testing for this risk. In order to assess capital adequacy, this means both the financiers and the regulators must be able to identify and price the risk.

In the pensions arena, trustees face new legal duties to disclose how they deal with stewardship and financially material ESG matters. The UK’s Pensions Regulator has said climate change is a core financial risk that trustees will need to consider when setting investment strategy. Therefore, this means that UK pension funds will be increasingly aligned with their Northern European and Australian counterparts, who have long-since seen good management of environmental, social and governance risk as a prerequisite to any allocation or capital to an investment intermediary[2].

Trustees are duty-bound to consider the financial implications of their decisions, which includes the financial risk associated with climate change, and presumably the financial risks associated with social and governance issues. Beyond the requirement to consider and disclose how they deal with these issues, pension trustees in England now also have case law to consider[3]. According to legal firm Charles Russell[4], pension trustees may also potentially take into account non-financial issues if:

the trustees have good reason to think that the scheme members hold the relevant concern; and

the decision does not involve significant financial detriment.

Measurement, Reporting and Verification

In order to properly take the financial implications of these issues into account, and to reflect the wishes of their members with regard to the non-financial implications, investors will need reliable measurements for both.

There can be no doubt that there has been a dizzying array of certifications and methodologies, which can be baffling for the well-meaning investor or asset owner, so much so that a not-so-mini-industry in advice and compliance support has emerged[5][6], including specifically within the real estate sector where a growing number of multi-disciplinary and boutique firms compete for data management, reporting and verification mandates.

In the real assets investment world – which we should remember is underpinned by increasingly globalised capital flows – voluntary certifications and standards abound for assets, portfolios and organisations. They include myriad competing and overlapping rating and certification systems, standards, benchmarks and indices. Some of these are particular to local markets, but many compete in an international context. Backing the right horse, each of which has its own inherent bias, can be a significant challenge for asset owners and managers alike, which is a key reason behind the decision of many to use multiple systems for the same purpose, often at considerable cost.

These systems have no doubt served an important purpose, and will continue to be used in the medium term, but many may require significant revision once regulatory standards (such as those in train in the EU), and accounting standards (such as those put forward by the Sustainable Accounting Standards Board)[7] come into widespread usage.

In the same way that investors and analysts can rely upon audited financial statements and regulated reporting of financial performance, similar levels of trust must be built into the reporting and verification of environmental and social performance. If companies and intermediaries want to access the wall of capital represented by the TCFD, which now has the support of over 1,000 organisations[8] controlling balance sheets totalling $120 trillion[9], or the Climate Action 100+ which represents some of the world’s largest pension funds with over $40trn in assets[10], then they must report independently verified ESG performance. Otherwise they may find themselves capital starved as the market moves forward.

There can be no doubt that a global approach is required, increasing common understanding across different products, sectors and across the ESG issues[11]. The result must be to facilitate and direct the flow of capital, not to confound it.

Comparison

The emerging consistency in approach to labelling of products and measurement of environmental and social risk management introduces for the first time the possibility of widespread direct product and manager comparison. Investors and consultants will be able to see which intermediaries and investee companies are able to manage environmental and social risk well, alongside financial risks. It will become clear who can deliver and who can’t. Capital allocations will follow.

Comparison of relative performance of risk managers will become even easier as the EU introduces its new ‘PACT’ benchmark standards – introducing clear standards for benchmarks to compare the performance of ‘Paris Aligned’ and ‘Climate Transition’ investments. Intermediaries who are marketing environmentally-focused sustainable and impact products will inevitably be compared to these new benchmark standards, and their strategies will be compared not only to those of other managers, or to ‘brown’ investments, but also in terms of their alignment to the 1.5 degree pathway (PA) and the 2 degree pathway (CT). The recently launched Carbon Risk Real Estate Monitor (CRREM)[12], funded under the EU’s Horizon 2020 programme with additional support from investment institutions including APG, PGGM and Norges Bank Investment Management, is a notable example of a tool intended for precisely this purpose, helping asset owners identify and quantify stranded asset risk.

Issuers of real assets and alternative investment products which are seeking to ride the growing wave of capital seeking sustainability and impact would do well to ensure their products meet the requirement for inclusion in these benchmarks, and indices which will no doubt develop around them. These will soon become a very easy route for capital allocators.

Product innovation

Rating Agencies

UNPRI has shown that ESG factors are relevant to investors’ view of credit risk, but ratings agencies still tend to look at ESG as a separate issue, even providing separate ESG rating services[13][14][15]. In future we should expect that these risks are seen as integral to all economic activity and, therefore, they should also be integrated into all credit ratings.

ESG in credit risk analysis is seen as a useful tool to manage downside risks but increasingly appreciated as a way to generate alpha. Governance is a relevant credit factor for all issuers. The materiality of environmental and social factors depends on their severity and on an issuer’s sector and geography.

Lending

In the second article in this series we learned about the RCF used by GPE to finance environmental improvements to its portfolio, judged against 3 environmental KPIs. If these are met, the rate on the loan will drop by 2.5 basis points, and GPE will give the difference to charity. If they are not met, then the lenders’ rate will remain the same and GPE will still make the donation. This is a clear acknowledgement by the lenders that management of ESG risk is fundamental to credit risk, and therefore a reduction in this risk can be tied to a reduction in the rate they demand for their lending.

This innovation could go further. KPIs are not traditional loan covenants which would cause the bank to step in, perhaps to renegotiate their rate, call in the loan, take security over assets or demand remedial action by management. Banks do have both operational covenants, such as requiring borrowers to file their accounts and pay their taxes on time, and maintain adequate insurance. Banks could request covenants related to maintaining or improving ESG performance.

If penalties for breach of ESG covenants led to financial penalties for borrowers, then it could potentially frustrate the original intended “use of funds”. But the same is true of all project finance, and in that market banks are not afraid to use milestones and covenants to manage the risk which they take on. It seems there is room for the lenders to go further in sustainable and impact lending, and this would be welcomed by shareholders. Thanks to shareholder activism, Lloyds has committed to halving the carbon emissions related to its loan book, and Barclays has come under pressure to phase out all lending to fossil fuel companies[16].

Securitisation

In Part II of this series, we learned that Generali has developed a framework for green insurance linked securities [17] which would see both the freed-up capital and proceeds of ILS being used for further ‘green’ investment. Banks could add these concepts to their ‘green bonds’ – thereby expanding the additionality and impact of the securities they issue, rather than simply passing on their already ‘green enough’ assets. Likewise, this concept could be expanded to social impact bonds.

Collaboration – across debt, equity and insurance

Since banks and borrowers are increasingly looking to price ESG risk into the pricing of debt facilities, the cost of failing to meet ESG covenants or KPIs will be more visible. Borrowers’ ability to meet these KPIs will also be impacted by climate change, for example demand for heating and cooling going up as weather becomes more extreme. One can see that the weather hedging products which the insurance and reinsurance industry regularly provide could help borrowers to isolate the ESG risk which they control, and “back out” the risk that they don’t. This could even allow borrowers and lenders to agree more challenging covenants.

Weather hedging products traditionally used in the agriculture and construction sectors to manage the risk of crop failure or delays in completion and are now being used to help de-risk the project financing and ongoing financial performance of renewables. There could be space for further innovation here, with insurers following the banks’ lead and giving preferential pricing for sustainable or impact weather cover. For example, covering the weather and climate risk on the construction of sustainable assets in real estate, social and economic infrastructure.

The Sierra Re catastrophe bond which completed in January 2020 was the first parametric catastrophe bond to cover earthquake risks embedded within a portfolio of mortgage investments[18]. This concept could be incredibly helpful to lenders and investors alike, allowing them to price and manage ESG risks across their portfolio.

The next 5 years

The world of sustainable and impact investment is developing apace. Those intermediaries which understand the direction of travel for the regulation of environmental and social risk management, and the redirection of capital which will follow, stand to gain a great deal. Those who fall behind will find themselves with decreasing prices in increasingly illiquid assets.

https://www.hillbreak.com/wp-content/uploads/2020/05/abstract-art-abstract-painting-colorful-abstract-painting-2014085.jpg483640Jon Lovellhttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngJon Lovell2020-06-02 06:00:522020-06-03 10:17:21IMPACT FINANCE SERIES: Part IV – The Future

In London, some property owners are in the vanguard of innovation in ‘green’ debt finance. In July 2019, Lloyds provided Blackrock with a £200m loan to finance energy efficiency improvements in the Blackrock UK Property Fund[1]. Later that year, Derwent agreed a £450m revolving credit facility (RCF) of which £300m[2] was designated as ‘green’ and will fund the construction of efficient buildings and improvements to their existing assets. CBRE Global Investors followed in March 2020 with a £60m green RCF to fund specific energy improvements to an industrial asset[3]. These facilities are utilising the “Use of Funds” concept which is embedded in the IFC’s principles for green bonds[4] and the LMA’s principles for green loans[5].

By February 2020, GPE had taken this innovation one step further by agreeing an RCF which was not only linked to the proposed use of funds for environmental purposes, but also includes financial downside risk for GPE if environmental outcomes are not delivered[6]. GPE has to hit KPIs on energy usage and biodiversity across its portfolio, and embodied carbon in its new buildings and major refurbishments. If GPE hits the targets, then the margin on the facility will decrease by 2.5 basis points; if not it will increase by the same amount. Either way, the difference will be given by GPE to registered charities focused on environmental issues. This is clearly a genuine financial incentive for GPE to hit its ESG targets and a clear acknowledgement by the lenders that management of ESG risk is fundamental to credit risk. Therefore, a reduction in ESG risk can be tied to a reduction in the interest rate attached to the loan.

The understanding that ESG risk and credit risk are intrinsically linked is not new. Since 2016, Lloyds has offered discounts of up to 20 basis points for clients meeting sustainability targets[7]. Similarly, since 2017, ING has offered sustainability improvement loans for corporate clients, providing a lower interest rate for improved sustainability performance[8]. The integration of ESG risk to the pricing of credit is clearly growing: GPE’s lenders included Santander, NatWest, Wells Fargo, Lloyds Bank plc and Bank of China. Others will follow.

Financiers are also seeking to take these innovations beyond the corporate market. The Green Finance Institute has convened the Coalition for the Energy Efficiency of Buildings to bring lenders, builders, advisers and government together to accelerate capital flows towards retrofitting and developing UK homes to net-zero carbon, resilient standards.[9] This will require not only innovation and a willingness to try a number of approaches, but also resilience and a willingness to learn lessons from failure. There are obvious examples.

The UK Government previously created the Green Deal Finance Company: a lending structure which turned builders into loan originators and energy companies into debt collectors. It failed – both financially and in its mission to catalyse energy efficiency improvements across the UK’s housing stock[10][11]. The idea had potential, but warnings were ignored and the ultimate method and structure of implementation were fatally flawed.

‘Green’ Debt Securitisation

Other innovations in the residential market have been more successful. In the US, Fannie Mae (or FNMA, the Federal National Mortgage Association) launched its Multifamily Green Financing Business in 2010. This offered ‘advantageous’ lending terms to owners of multifamily rental properties who were willing to commit to target reductions in energy and water consumption. Since 2012, Fannie Mae has raised additional finance by using these loans as the basis for green mortgage-backed securities (MBS) and became the world’s largest green bond issuer with more than $50 billion issued by Fannie Mae by the end of 2018[12]. Various private lenders now offer preferential mortgage rates to borrowers buying highly energy efficient homes, and low interest loans for those wishing to make energy performance upgrades[13].

The natural progression in the private sector is, therefore, for more lenders to issue green MBS (mortgage backed securities). This is already happening, including issuers such as Natixis and Goldman Sachs in the commercial mortgage market[14][15] and Obvion (part of Rabobank) and NAB in the residential space[16][17]. In both markets, the securitisations tend to be labelled “green” on the basis that the underlying buildings against which they are secured are high quality from an energy performance perspective. The “green-ness” can of course be debated in that most building ratings are based on the assumed performance of the building based on a hypothetical reference model. Actual performance in use may – almost invariably does – differ. Likewise, these ‘green’ badges tend not to take into account embedded carbon related to the building process and materials used for construction, nor the other environmental implications of the building (such as locational implications for transport, impact on green space or biodiversity, water and waste efficiency etc).

However flawed the labelling, this is a start. As we saw in the first article in this series, regulators and industry bodies are now stepping in to clarify and clean up the labelling. So, what of this trend for ‘green’ mortgages and the related securitisations? Do they help to decarbonise real estate stock? Probably not. The assets underlying these structures are being built for low and zero carbon performance due to increasing regulation and occupier demand. But they do help investors to understand what they hold. If you are holding a portfolio of MBS of which only 5% is labelled ‘green’, then you can assume that the other 95% is not only underperforming from an environmental perspective, but it is also exposed to significant regulatory risk and is off-trend in terms of what occupiers increasingly expect. Thus, the 95% is exposed to pricing and demand risk, possibly even stranded asset risk (which undermines the residual value assumptions which will have been made by the originator). Investors can now see clearly where some material financial risks sit in their portfolio, and therefore start grappling with quantification, disclosure and reduction of these risks.

Energy performance is not the only relevant risk. Beyond the “in use” energy efficiency of buildings, real assets can be exposed to risk around water and waste efficiency, extreme temperatures and weather events, and other physical climate-related risks (flood, wildfire, mudslide, coastal erosion, rising sea levels). Very few asset owners have a strong understanding of the full financial implications of these risks. All climate-related risks which lead to financial risk must be considered by the 1,000 banks, asset managers, pension funds, insurers, credit rating agencies, accounting firms and shareholder advisory services which have declared their support for the Task-Force on Climate-related Financial Disclosures (TCFD)[18] and which control balance sheets totalling $120 trillion[19]. The labelling of certain assets as “low” risk on one climate-related measure should serve as a red flag for investors with regard to the rest of their portfolio, and the rest of the risks to which they are exposed.

Social, Green, Sustainable & Impact Real Estate Funds

There has also been significant growth in the use of ‘sustainable’ and ‘impact’ labelling and messaging in real estate equity funds (albeit ahead of the formalisation of the term ’sustainable’ in EU legislation). Here too we see significant variance in the type and extent of environmental and social risk management available to investors.

Pension funds – especially the very large funds – are becoming arguably more sophisticated in this space than some of the intermediaries which dream of building lasting relationships with them. Evidence of this can be seen in the levels of sophistication of the sustainability policies these organisations publish, and their increasing appetite for co-investment, where they can exercise a greater degree of strategic control of directly held assets.

Mainstream balanced or sector-focussed funds targeting the institutional market have tended to include at least some commentary on their sustainability performance in either their marketing documents or investor reporting (albeit often in the form of one-off development or refurbishment case studies rather than wholesale portfolio improvement programmes).

Some funds claim they are good for society because the assets themselves have intrinsic social utility. Classic examples include affordable and social housing, and social infrastructure assets such as care homes, medical facilities and schools. Some of these funds are taking the development risk and creating new assets which can be used to serve under-served communities. However, others are simply buying standing assets and often benefitting from long-term, government-backed revenues. One has to question how these managers would answer the third impact management principle which requires that they establish their own contribution to the achievement of the impact.

In the environmental space, there tends to be a more active approach. The Columbia Threadneedle Low Carbon Workplace Fund, launched in 2010, actively seeks office assets which are in need of refurbishment in order to improve their carbon performance. The Fund’s objectives include that occupiers should either meet best practice emissions benchmarks or demonstrate year-on-year improvements.

The Triodos Real Estate Fund, launched in the Netherlands in 2004, sought to improve the performance of its portfolio to the point of reaching net zero carbon emissions (with the use of some renewable energy generation and carbon offsetting). Likewise, the Credit Suisse (Lux) European Core Property Fund Plus, launched in 2016.

It will therefore be very useful for investors to look at labelling and marketing materials again once the new EU regulations come into force. Some funds may have to dampen their marketing claims, and potentially even change their fund name. Others who may not have felt comfortable in using the term ‘sustainable’ given the level of debate in the market may now step forward with more confidence. Likewise, investors should be expected to make reallocations in favour of those funds which they can now clearly identify as ‘sustainable’.

The Future

The real estate market has clearly been innovating, but what next? In the next and final part of this series we will explore what the future of the market might look like, potential new product innovations and the joining up of the sustainable and impact equity, debt and insurance financing worlds. We will also consider how this might create winners and losers, and dramatically alter our pricing and management of environmental and social risk.

https://www.hillbreak.com/wp-content/uploads/2020/05/abstract-art-abstract-painting-colorful-abstract-colorful-2019468.jpg480640Caroline McGillhttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngCaroline McGill2020-05-31 07:14:042020-06-03 10:13:24IMPACT FINANCE SERIES: Part III – The Assets

In the first article of our Impact Finance series, we sought to demystify the various terms used to describe different investment styles (responsible, sustainable, impact and transition) and themes (environmental, social, climate and green). Here, we move on to consider how the various parts of the capital markets isolate, prioritise and manage specific ESG risks, and how these risks and investments are interrelated through equity, debt and insurance.

Increasing investor appetite

As awareness of social and environmental risk has increased, so investors are increasingly willing to publicly signal their intention to be responsible, and invest in sustainable and impact financing products. What was once widely seen as a niche investment area for “soft” capital, is increasingly understood to deliver commensurate (or better) returns on investment [1][2], while actively managing and mitigating environmental and social (ES) risks which have previously been ignored.

The Task Force on Climate-related Financial Disclosures (TCFD) has the support of organisations controlling balance sheets totalling $120 trn[3], of which nearly $12 trn[4] is in the private sector. These supporters include the world’s top banks, asset managers, pension funds, insurers, credit rating agencies, accounting firms and shareholder advisory service providers. The Climate Action 100+ represents some of the world’s largest pension funds with over $40trn in assets. UNPRI signatories include asset owners and investment managers with $90trn under management[5].

Product range

Where the capital goes, financial innovation follows. An ever-increasing array of financial products which claim to address ES risks are now available. The product suite is vast and varied and covers the spectrum of equity, debt, insurance and bespoke contractual instruments. Products now exist to isolate and price ES risks. To name but a few:

weather hedging products for agriculture and renewable energy producers;

insurance linked securities for property owners and banks exposed to the cost of wildfire, floods, hurricanes, earthquakes, and other natural catastrophes;

contracts for difference to protect renewable energy producers from energy price risk;

social impact bonds taking the risk of criminal reoffending rates;

an array of loans and bonds, sovereign and corporate, which are intended to fund sustainable and impact investments; and

securitisation of sustainable and impact debt.

Risk capital being put to work to take environmental and social risks is, in principle, a good thing. The more this market grows, the better the cost of these risks will be understood, and factored into decisions by governments and private sector actors alike. The more capital flows into this market, the more regulators and industry bodies will work to formalise and standardise the labelling and reporting which allow investors to understand the impact their capital has, and to trust the sustainable and impact products in which they have clearly signalled their desire to invest.

Capital flows

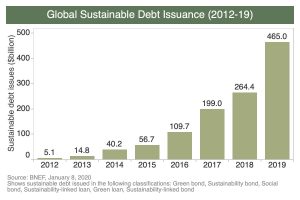

However, the flow of capital is still a trickle rather than a gush. In October 2019, the total amount of sustainable debtin global markets surpassed $1tn, according to an estimate from BloombergNEF[6]. This is nowhere near the tens of trillions under the management of the TCFD, Climate Action 100+ and UNPRI supporter.

The amount of equity which is flowing into specifically sustainable or impact products is harder to pinpoint, but it is growing rapidly. In early 2018, the global sustainable investment alliance estimated that total global sustainable investment had reached $30.7 trillion, a 34 percent increase in just two years[7]. According to the Global Impact Investing Network’s Annual Investor Survey, the impact investments managed by their survey respondents has been doubling year on year, from $114 billion in assets in 2017 to $228 billion in 2018, and had reached $502 billion by April 2019. In March 2020, Morningstar identified over 300 open-ended and exchange-traded funds available to US investors that have sustainable investing at the core of their investment strategy – of which about two thirds were equity funds[8]. The signatories of the Impact Principles declared $182bn of their AUM to be in Impact investments, of which $165bn was in government owned development banks but only $17bn in the private sector[9].

The exponential growth in sustainable and impact investment should be no surprise given that the investors who have signed up to Climate Action 100+ represent some of the world’s largest pension funds with over $40trn in assets[10]. These investors are seeking to make a positive environmental impact by engaging with companies “to ensure that they are minimising and disclosing the risks and maximising the opportunities presented by climate change”.

While the vast majority of equity investment is done through listed equities, traded on exchanges which don’t classify the investee companies as sustainable, impact or otherwise, there are a growing number of indices which select investee companies based on some sort of ESG screening criteria (e.g. excluding fossil fuel producers). However, indices which screen out the “worst” offenders don’t tell us much else about the sustainability or impact of those they include – nor do they tell us the motivations of the shareholders in making those investments. There is no doubt, however, that companies are seeing increasing pressure from some of the world’s largest investors to address the ESG risks in their businesses. Larry Fink, Chief Executive of Blackrock (which has $7trn under management) has said publicly that “Climate change has become a defining factor in companies’ long-term prospects… awareness is rapidly changing, and I believe we are on the edge of a fundamental reshaping of finance.”[11]

In the insurance linked securities space, the first quarter of 2020 was the strongest Q1 on record for total catastrophe bond issuance, with USD3.8 billion issued[12]. However, less than half of all natural catastrophe losses are insured and this is worse in developing and emerging countries where the proportion of insured losses is still well below 10% and often almost zero.[13] There is clearly room for more risk capital in the insurance market. However, natural catastrophe events such as hurricanes, typhoons, floods and wildfires have had a significant effect on reinsurers (who take risk from insurers). As a result, many investors have experienced losses and some have withdrawn from the space[14].

Are these losses an indication that environmental and social risks are unfinanceable? As any good underwriter will tell you, taking risk is how returns are made – as long as you correctly price the risk. This means equity investors must demand an appropriate ROI, bankers must charge enough interest to cover expected loss, and insurers must charge sufficient premia. The fact that investors taking these types of risks include long term investors like insurers and pension funds sitting alongside hedge funds should be a warning sign. Someone’s view of pricing versus risk must be off.

Product Innovation

In the insurance space, Generali has developed a framework for green insurance linked securities [15]. This is intended to enable all insurance linked securities, not just those relating to natural catastrophe risk to claim the ‘green’ badge. For example, insurance linked securities (ILS) are also used in life and auto insurance. When insurers issue an insurance linked security, the investor takes on the relevant risk of claims arising, as a result the insurer doesn’t need to hold as much capital in reserve. In Generali’s green ILS framework, the insurer would use the freed-up capital to insure further environmental risks. In addition, when the investor takes on the insured risk, they place collateral in an SPV (special purpose vehicle) in case claims do come in. This collateral is invested, typically in treasuries and other very low risk assets. Generali’s proposal is that the SPV use this collateral to invest in ‘green’ financing.

IBRD (part of the World Bank) is already doing something similar. IBRD is insuring natural catastrophe (‘natcat’) risk for Mexico, and has issued a hybrid natcat development bond. The natcat risk is transferred to investors (subject to specific risk parameters), and the IFC uses the collateral to invest in international development. [16]

Weather hedging products traditionally used in the agriculture and construction sectors to manage the risk of crop failure or delays in completion are now being used to help de-risk the project financing and ongoing financial performance of renewables.

In the debt markets, social and sustainability bonds are on the up. Where issuers and investors have previously struggled to scale up the use of social bonds, partly due to difficulties in impact baseline and improvement measurement, this seems to show that where there is an imperative then an investment solution can be found. HSBC expects issuance of social and sustainability bonds between $100bn and $125bn this year[17], up from a total of $61bn ($17bn and $44bn respectively) in 2019[18]. Its estimate of green bond issuance this year is $225 billion – $275 billion (in line with 2019’s $262bn[19]). This expected uptick on social and sustainability bonds is reflective of several large pandemic-related bonds from development banks.

The range of debt products is also expanding, with various London property owners now utilising revolving credit facilities for environmental purposes (more on this in our next Article in this series)[20][21].

The Sierra Re catastrophe bond issued in January 2020 was the first parametric-based catastrophe bond to cover the risk of earthquakes in a portfolio of mortgage investments.[22] This is unusual in that it’s a rare example of insurance-type products being issued by lenders in order to manage their own exposure to ESG risks.

However, while innovation can be positive, all actors and investors should be sure they understand the risks they are exposed to, what they take on, what they can manage, and ultimately what they pass on. Insurers and investors in natural catastrophe risk and weather derivatives are relying upon historical data and complex stochastic models to price risk, and don’t always get it right. Traditional lending models work out expected loss by looking at very different data such as credit ratings, sector, size and location of business, and financial metrics. These models also fail.

Arguably, reinsurers beginning to price and take ESG risk from lenders improves the management of risk in the financial system. However, we should be wary of any actors who originate risk they do not understand. The idea of lenders blindly trusting reinsurance markets as they did credit ratings and debt securitisation markets is more than a little terrifying. Losses do occur and if pricing or judgement of risk is wrong then the capital reserved may not be sufficient to cover those losses. This is damaging to the whole system – and puts the financial wellbeing of the insured, the bank, the intermediary and the ultimate investor at risk. The providers of capital, the originators of risk, the ratings agencies and the regulators who supervise the entities and the financial system all need to understand the ESG risks involved.

The Assets

Some property owners are in the vanguard of innovation in sustainable and impact financing. In Part III of this series, “The Assets”, we explore how the real estate market is using and driving sustainable finance markets, and the financial risks of falling behind.

https://www.hillbreak.com/wp-content/uploads/2020/05/abstract-art-abstract-painting-amber-lamoreaux-modern-art-2017798-2.jpg480640Caroline McGillhttps://www.hillbreak.com/wp-content/uploads/2021/02/hillbreak-green.pngCaroline McGill2020-05-29 08:13:042020-06-03 10:16:30IMPACT FINANCE SERIES: Part II – The Markets

In this series of articles we explore the sustainable, responsible and impact investment landscape.

Beginning with “Part I – The Jargon” we attempt to break down the language barrier and explain what is meant by terms like “Impact”, “Green”, “Sustainable” and “Responsible” when it comes to investing.

In “Part II – The Markets” we explore how the various parts of the capital markets isolate, prioritise and manage specific climate and social risks, and how their risks and investments are interrelated through equity, debt and insurance.

“Part III – The Assets” explores how the real estate market is using and driving sustainable finance markets, as well as the financial risks of falling behind.

“Part IV – The Future” builds on these topics to consider how the sustainable investment market might create winners and losers, drive new financial products and dramatically improve our management of risk.

So, beginning with Part I – The Jargon:

What counts as Sustainable / Responsible / Impact Investment?

I have advised on “impact investing” since 2009. The global financial crisis had created an opportunity. For me personally, it meant working with the UK government to advise on business finance markets, and specifically how to use them, and change them, to speed the economic recovery and thereby limit the social implications of the crisis. This included acting in a lead advisory capacity on the establishment of the £3bn Green Investment Bank, the £1bn British Business Bank, and the £200m London Green Fund.

Since then, I have worked with lots of investors and intermediaries seeking to make an impact while they make a financial return. I have also seen others accused of “green-washing”, or more recently “SDG-washing”, a term applied to those who seek superficial alignment to the UN Sustainable Development Goals in their marketing collateral and disclosures. So, how can an investor or shareholder make informed allocation decisions and know what impact they are really having?

Looking back to the early days of my career, one of my key indicators as to whether an organisation was serious about impact investment was whether my meetings included the client CFO or CIO. If not, it was unlikely that much would be done about any good intentions we might explore. Increasingly – almost invariably – meetings now involve CEOs, CFOs, CIOs, or the whole board. Business leaders and their shareholders are getting passionate about social and environmental risks and opportunities. CFOs and CIOs are getting clearer evidence of the potential costs that social and environmental risks pose for their bottom line. As a result, ESG and responsible investment teams are under increasing pressure to advise on these risks and help their organisation, and their clients, to capitalise on the opportunities.

Without doubt, the jargon is myriad and confusing. Every-day words are now being used by ESG specialists to mean very specific things, which might not be immediately obvious to others. The lexicon is growing and changing, as is the related regulatory framework, especially in Europe. A few of the key investment styles and themes to master, and which we characterise below, include:

Investment Style

Investment Theme

Sustainable

Responsible

Impact

Transition

Environmental

Social

Climate

Green

These terms are not mutually exclusive, and the overlap may be less than you think.

Investment Styles

Sustainable

The EU has helpfully been setting about formalising the way we use these terms with respect to financial disclosures and investments[1]. For the EU, ‘sustainable investment’ must:

contribute to environmental objectives in a measurable way, or

contribute to social objectives, and

do no significant harm to any social or environmental objectives, and

follow good governance practices.

This is significant as it ties all three Environmental, Social and Governance (ESG) pillars into the concept of sustainability. It also borrows the concept of non nocere, meaning “do no harm”, from the hippocratic oath familiar to medics around the world.

Under new EU rules, a product cannot be marketed as environmentally or socially sustainable based on just one or two factors. It must effectively be neutral or positive on all other environmental and social factors, and “good” from a governance perspective, in particular with respect to sound management structures, employee relations, remuneration of staff, and tax compliance.

Back in 2015, the UN launched the increasingly familiar Sustainable Development Goals[2], an expansion and development of the former Millennium Development Goals. Significantly, whilst developed for the principal purpose of directing and aligning intragovernmental policy and programmes towards global societal challenges, they have found significant appeal amongst the investment community, effectively acting as an off-the-shelf taxonomy. In this sense, they highlight a number of ESG themes and factors as being inherent to the “sustainable” investment label. These goals aren’t worded identically to the EU’s objectives and examples, but they do align.

UN SDGs

Responsible

The UN Principles for Responsible Investment[3] outline how ESG factors should be part of investment decisions and active ownership. Driven by investors, this again seeks not to duplicate the work of others in defining the ESG issues, but instead defines how the issues should be treated by investors and intermediaries, in terms of both investment process and related corporate behaviours:

Summary Principles

Translation

Incorporate ESG issues into investment analysis and decision-making processes

Put your money where your mouth is

Be active owners and incorporate ESG issues into ownership policies and practices

Do it across your business, not just in a few token investments

Seek appropriate disclosure on ESG issues from the recipients of capital

Hold the organisations you fund to account

Promote the Principles within the investment industry

Get other investors and intermediaries on the same page

Work together to enhance our effectiveness in implementing the Principles

Apply some collective pressure and share best practice

Report on our activities and progress towards implementing the Principles

Keep each other honest

It is quite commonly understood that responsible investment therefore relates to the integration of material ESG factors into investment processes and decision-making, such that harm is avoided and ESG risks are mitigated. At the heart of the UN PRI is the pursuit and delivery of competitive, risk adjusted returns, recognising that material ESG factors that are not considered and managed effectively will likely result in weaker financial performance. The market evidence to support this theory now borders the irrefutable. The inherent bond between responsible investing and fiduciary duty is, as a result, understood by the vast majority of informed investment professionals.

Impact

According to the Global Impact Investing Network[4], impact investments are made with the intention of generating positive, measurable social and environmental impact alongside a financial return.

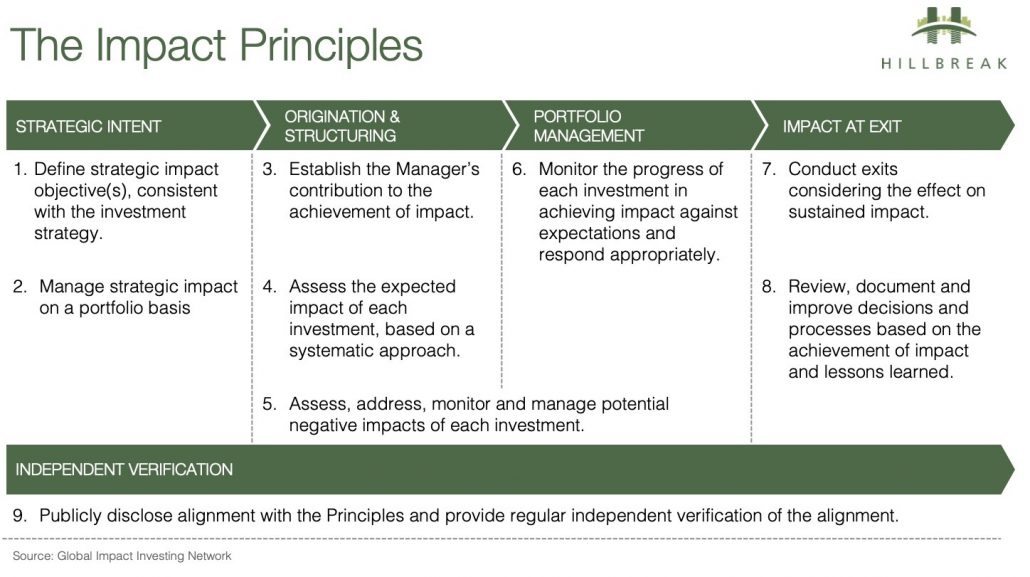

The IFC has augmented this by developing a set of impact investing principles[5] backed by 60 public and private investors to define how this should be done in practice. This adds specificity about the requirement for measurement, management, verification and reporting of impact. This is clearly about more than just passively taking assets which are “good enough” or making minor improvements. It denotes a more active, intentional and additive approach to investing risk capital to mitigate environmental and social risk and deliver positive outcomes.

The Impact Principles

Notably, these principles don’t include the “do no harm” requirement of the EU, or the comprehensive industry engagement and investor reporting requirements of the UNPRI. Nor are they specific about whether only the intended positive impact or also the potential negative impacts should be measured and reported.

The Impact Management Project[6], which includes the GIIN, IFC and PRI has gone further to clarify that impact management should be “the ongoing practice of measuring and improving our impacts, so that we can reduce the negative and increase the positive”. Investors should therefore expect to see measurement of the good and the bad, and judge the performance of their investments (and their intermediaries) on this basis.

Transition

Related to ‘impact’ investing is the term ‘transition’, typically used in the debt markets as labelling for ‘transition finance’. This has come into use as a descriptor for investments seeking to enable improvements in the climate and energy performance of assets and businesses. The climate transition is usually referenced to specific targets to reduce GHG emissions and limit the expected global temperature increase to 1.5 or 2 degrees. The targets to which these investments align are not necessarily consistent. Often, they align to the targets set out in the Paris Agreement and reiterated by national governments. However, increasingly, local authorities and businesses are setting their own, more ambitious targets, either increasing their level of ambition in terms of quantity or timing of emissions reduction. Similarly, the energy transition is commonly understood to mean a transition away from fossil fuels (or to cleaning them up, such as through carbon capture and storage) and towards renewable and sustainable energy sources. In the space of transition finance there is, therefore, no standard benchmark or level to which the investments must perform from an ESG perspective. They must simply seek to make a contribution.

‘Transition’ is also used in the context of a ‘just transition’. This concept has been developed by the UN Sustainable Development group[7] and links the climate and energy transition to the societal goals set out in the SDGs. Under this model the climate transition must not be achieved at the expense of social progress and should actively seek to contribute to the societal goals.

Investment Themes

Environmental

The EU’s approach to environment – set out in its draft regulation for the establishment of a framework, or ‘EU taxonomy’ to facilitate sustainable investment – is as one might expect. It defines six objectives and cites several issues as examples of factors one might consider:

the sustainable use and protection of water and marine resources;

the transition to a circular economy;

pollution prevention and control;

the protection and restoration of biodiversity and ecosystems.

use of energy, renewable energy, raw materials, water and land; or

production of waste, and greenhouse gas emissions; or

impact on (or loss of) biodiversity and the circular economy

climate change;

the global overconsumption of resources;

food scarcity;

ozone depletion;

ocean acidification;

the deterioration of the fresh water system;

land system change; and

the appearance of new threats, such as hazardous chemicals and their combined effects.

One could be forgiven for thinking, therefore, that environmentally sustainable investments simply need to contribute to one or more of the environmental objectives, be neutral socially, and be well governed. Not quite! Controversially, the EU goes further. As well as citing specific standards and guidelines from the OECD and UN[11] which must be met with regard to social and governance issues, it requires that the investment “complies with technical screening criteria” on the environmental side.

The technical criteria established for environmental sustainability have been criticised for a couple of key reasons. Firstly, the regulations use existing technical measurements and standards to define what will meet the threshold for products and activities to be labelled as environmentally sustainable. This is fairly easy mud to throw. In a complex space where no one size fits all, most specialists can see significant scope for improvements in the global benchmarks (such as GRESB[12]) and EU regulations on Energy Performance Certificates for buildings[13]). Of course, these regulations and standards are not perfect, but they are established tools which are available now and can be improved and built upon in future. So, the structure of the EU’s approach makes sense, and leaves room for improvement as measurements and standards become more effective over time.

The second criticism is that the technical standards set too high a hurdle, including only very green (or “dark green”) investments, and excluding other activities which would contribute to the objectives, but not to the same degree. This criticism misses the point. A key objective of the legislation is to provide an easy flag for investors. The “sustainable” label in the EU seems intended to highlight those investments which are ostensibly “good enough” or “safe enough” in terms of having limited exposure to ESG risk. By definition, one would expect these investments to exclude those where the investors’ allocation of capital might be expected to have a negative impact in terms of environmental or social change. Arguably, also by definition, one would expect these investments to exclude the majority of existing investments, including those intended to make only partial or limited improvements to the management of environmental or social risks . This label is effectively a ‘safety’ label, or a hallmark indicating high ESG quality assets for positive screening purposes, and not about ESG risk management and quality improvement across a whole portfolio.

Admittedly, the EU intention to establish ‘brown’ criteria within the taxonomy at a later date, capturing those activities that are deemed to cause significant environmental harm, would enhance the potential application of the framework within the market by bringing into play a broadly accepted negative screening threshold too.

Social

The EU has indicated that a comparable approach will be taken to defining socially sustainable investment, namely that the investment must:

contribute to social objectives, and

do no significant harm to any social or environmental objectives, and

follow good governance practices.

The social objectives which have been established to date are:

tackling inequality

fostering social cohesion,

improving social integration

improving labour relations

investing in human capital

investing in economically or socially disadvantaged communities.

Climate

Driven by regulators, and gaining private sector support, the Task Force on Climate-related Financial Disclosures (TCFD) has identified a number of financial risks as being “climate-related”. Its approach fits broadly with the intuitive, everyday interpretation of the word ‘climate’ as being related to carbon dioxide and other greenhouse gases in the atmosphere, and their effect on rising temperatures, sea levels, and extreme weather events. They don’t explicitly mention every single climate issue – notably scarcity of natural resources, air quality or biodiversity – but these are implicit factors which impact on the risks identified. This is not a shortcoming, rather a product of its approach: defining the financial risks (below) and opportunities, rather than duplicating work done elsewhere in defining the underlying issues. Rather sensibly, anything climate-related which exposes investors to financial risk should be considered when making climate-related financial disclosures. Therefore, those making the disclosures should have an eye on the issues and examples already outlined by the EU and UN.

Green

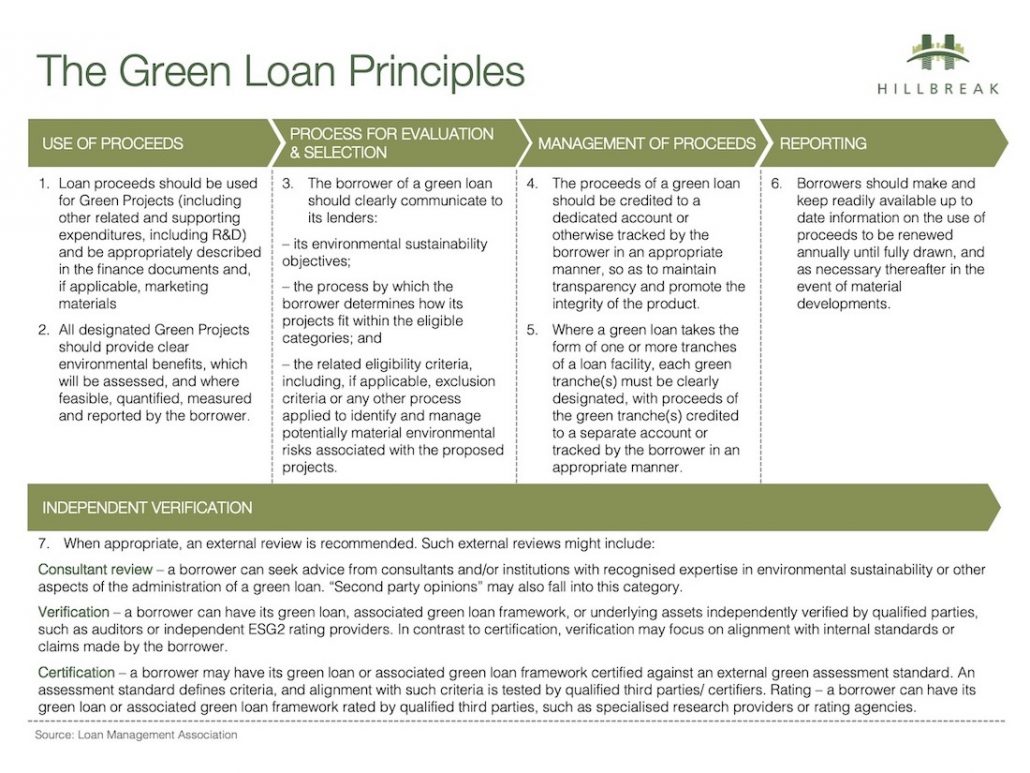

Much work has been done to set out how ‘green’ finance should be issued and managed, such as the Loan Market Association’s Green Loan Principles (below)[14] and the International Capital Market Association’s (reassuringly similar) Green Bond Principles[15].

Green Bond Loan Principles

As well as setting out the principles for how this form of finance should be done, both give examples of what might qualify as a ‘green’ use of proceeds, including such things as renewable energy, energy efficiency or ‘clean transportation’.

Surely, therefore, launching a Green Bond to finance more fuel-efficient vehicles would be green? But what if those vehicles were oil tankers, as with the Green Bond issued by Teekay Shuttle Tankers? Then, opinions differ[16][17] – some find any investment in certain sectors, such as fossil fuels, unacceptable. Others are willing to invest to “clean them up” as part of the transition to a less carbon intensive or ‘net zero’ future. So, is it enough to make something better, even if it’s still not going to end up fully or dark ‘green’? This is where the growing distinction between sustainable investment, and impact or transition investment is helpful.

Arguably this is impact or transition financing, not sustainable financing, and the use of the term “green” is an unhelpful badge. It is a label which is controversial and has covered all manner of sins in the past, allowing companies to claim “green” credentials while doing more harm than good, or while spending more on advertising how “green” they are than they do on delivering real environmental improvements within or through their business. It evokes environmental issues without giving any real indication as to the purpose of the deployment of the capital: taking lower or higher risk, being passive or actively managed.

Investments may be sustainable and have no impact (such as buying a building which already exceeds the EU’s technical quality threshold), or be sustainable and have impact (such as investing to improve a building to meet the technical threshold), or may have impact but not reach the threshold above which investments would qualify as “sustainable” under the EU lexicon. In short, the terms sustainable and impact are not mutually exclusive, nor is one confirmation of the other. An investment may be sustainable, impactful, both or neither. A clear understanding by all actors of the distinction between sustainable and impact investment should help investors know what they’re getting, and to start to ask how much impact their money really has – both positive and negative.

The Markets

Now that the terminology is maturing, and in many cases is being formally defined in legislation, we can start to understand how these terms have been used (and misused) in the capital markets. The lexicon is useful for investors seeking to isolate, prioritise and manage specific climate and social risks, and innovative stand-alone and inter-related products have emerged in the equity, debt and insurance markets. We explore these in Article 2 in this series.